The Public Provident Fund (PPF) is one of the safest investment options in India. It is backed by the Government of India, which means your money is completely secure. Apart from giving steady returns, PPF is also an excellent tax-saving option under Section 80C of the Income Tax Act.

What makes PPF even more attractive is that it falls under the rare Exempt-Exempt-Exempt (EEE) category. This means:

In short, you save tax when you invest, you don’t pay tax while your money grows, and you don’t pay tax when you withdraw. Let’s understand these tax benefits of PPF with simple examples.

| Benefit Type | Details |

|---|---|

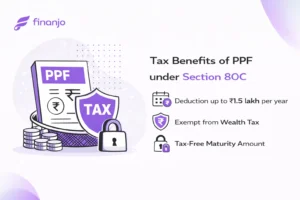

| Section 80C Deduction | You can claim tax deduction on deposits up to ₹1.5 lakh per year. |

| Interest Earned | The interest credited annually is completely tax-free. |

| Maturity Amount | The full maturity value (your investment + interest) is tax-free. |

| Status | Falls under EEE (Exempt-Exempt-Exempt) category. |

When you invest in PPF, the amount is eligible for deduction under Section 80C. This helps you reduce your taxable income and pay less tax.

By simply investing in PPF, you bring down your taxable income, which directly reduces your income tax liability.

The interest you earn on your PPF balance is added to your account every year and is fully tax-free. This is a major advantage compared to options like fixed deposits (FDs), where the interest is taxed.

This ₹8,520 gets added to your account balance and will also earn interest in the following years. Since it is tax-free, your money grows faster through compounding.

After the lock-in period of 15 years, you can withdraw the entire amount (your investment + accumulated interest). The best part is, you don’t have to pay any tax at maturity.

If this money were invested in a taxable instrument, a big chunk of the interest would go into taxes. But with PPF, every rupee is yours.

You can also use PPF for family tax planning. Accounts can be opened for your spouse or minor children. While the overall deduction limit is still ₹1.5 lakh under Section 80C, this strategy helps build a larger tax-free family corpus.

Even though the deduction is capped, the total money invested for your family grows tax-free and creates a strong financial base.

Section 80C offers multiple tax-saving options. Let’s compare:

This makes PPF one of the most tax-efficient choices for conservative investors.

It’s genuinely tax-free. Whatever you put in, whatever interest you earn, and whatever you get at the end none of it is taxed.

Yes. The money you put into PPF can be used to save tax under Section 80C, up to ₹1.5 lakh in a year.

No. The interest you earn just keeps adding up quietly without any tax cutting into it.

You don’t pay tax on it, but it’s still better to show it as exempt income when you file your return.

That’s fully yours. The entire maturity amount comes without any tax deduction.

No. There’s no TDS on PPF neither on interest nor on withdrawals.

Yes. As a parent or guardian, you can claim the tax deduction under 80C for that amount.

You won’t get the 80C deduction there. But the good part is PPF interest and maturity stay tax-free anyway.

No. Even the allowed partial withdrawals are tax-free.

For long-term savings, yes. FD interest gets taxed every year, but PPF grows without tax eating into your returns.

The Public Provident Fund (PPF) is one of the safest investment options in India. It is backed by the Government of India, which means your money is completely secure. Apart from giving steady returns, PPF is also an excellent tax-saving option under Section 80C of the Income Tax Act.

What makes PPF even more attractive is that it falls under the rare Exempt-Exempt-Exempt (EEE) category. This means:

In short, you save tax when you invest, you don’t pay tax while your money grows, and you don’t pay tax when you withdraw. Let’s understand these tax benefits of PPF with simple examples.

| Benefit Type | Details |

|---|---|

| Section 80C Deduction | You can claim tax deduction on deposits up to ₹1.5 lakh per year. |

| Interest Earned | The interest credited annually is completely tax-free. |

| Maturity Amount | The full maturity value (your investment + interest) is tax-free. |

| Status | Falls under EEE (Exempt-Exempt-Exempt) category. |

When you invest in PPF, the amount is eligible for deduction under Section 80C. This helps you reduce your taxable income and pay less tax.

By simply investing in PPF, you bring down your taxable income, which directly reduces your income tax liability.

The interest you earn on your PPF balance is added to your account every year and is fully tax-free. This is a major advantage compared to options like fixed deposits (FDs), where the interest is taxed.

This ₹8,520 gets added to your account balance and will also earn interest in the following years. Since it is tax-free, your money grows faster through compounding.

After the lock-in period of 15 years, you can withdraw the entire amount (your investment + accumulated interest). The best part is, you don’t have to pay any tax at maturity.

If this money were invested in a taxable instrument, a big chunk of the interest would go into taxes. But with PPF, every rupee is yours.

You can also use PPF for family tax planning. Accounts can be opened for your spouse or minor children. While the overall deduction limit is still ₹1.5 lakh under Section 80C, this strategy helps build a larger tax-free family corpus.

Even though the deduction is capped, the total money invested for your family grows tax-free and creates a strong financial base.

Section 80C offers multiple tax-saving options. Let’s compare:

This makes PPF one of the most tax-efficient choices for conservative investors.

It’s genuinely tax-free. Whatever you put in, whatever interest you earn, and whatever you get at the end none of it is taxed.

Yes. The money you put into PPF can be used to save tax under Section 80C, up to ₹1.5 lakh in a year.

No. The interest you earn just keeps adding up quietly without any tax cutting into it.

You don’t pay tax on it, but it’s still better to show it as exempt income when you file your return.

That’s fully yours. The entire maturity amount comes without any tax deduction.

No. There’s no TDS on PPF neither on interest nor on withdrawals.

Yes. As a parent or guardian, you can claim the tax deduction under 80C for that amount.

You won’t get the 80C deduction there. But the good part is PPF interest and maturity stay tax-free anyway.

No. Even the allowed partial withdrawals are tax-free.

For long-term savings, yes. FD interest gets taxed every year, but PPF grows without tax eating into your returns.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.