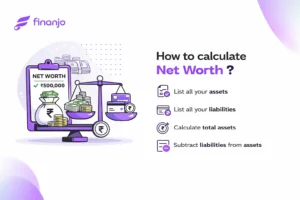

Net Worth is the difference between what you own (assets) and what you owe (liabilities). It shows your real financial position. Whether you are an individual, a family, or a business, knowing how to calculate net worth helps you track progress, set financial goals, and plan for the future with clarity.

In this guide, we explain the net worth calculation formula, break down what counts as assets and liabilities, share practical examples, show a sample net worth statement, and also cover why using a Net Worth Calculator online is the fastest way to get accurate results.

| Factor | Details |

|---|---|

| Definition | Total Assets – Total Liabilities |

| Assets | Cash, investments, property, gold, vehicles, retirement funds |

| Liabilities | Loans, credit card dues, EMIs, mortgages |

| Formula | Net Worth = Assets – Liabilities |

| Type | Can be positive (healthy) or negative (more debt than assets) |

The formula is simple:

Net Worth = Total Assets – Total Liabilities

Assets:

Savings & Investments = ₹10,00,000

Property = ₹40,00,000

Vehicle = ₹5,00,000

Total Assets = ₹55,00,000

Liabilities:

Home Loan = ₹25,00,000

Car Loan = ₹3,00,000

Total Liabilities = ₹28,00,000

Net Worth = 55,00,000 – 28,00,000 = ₹27,00,000 (Positive)

Assets:

Savings & Investments = ₹2,00,000

Property = ₹5,00,000

Total Assets = ₹7,00,000

Liabilities:

Loans & Credit Card Debt = ₹10,00,000

Total Liabilities = ₹10,00,000

Net Worth = 7,00,000 – 10,00,000 = –₹3,00,000 (Negative)

A net worth statement shows assets and liabilities side by side for clarity. Here’s an example:

| Assets | Value (₹) | Liabilities | Value (₹) |

|---|---|---|---|

| Cash & Savings | 2,00,000 | Home Loan | 20,00,000 |

| Investments (SIP, FD, Stocks) | 8,00,000 | Car Loan | 2,00,000 |

| Property | 30,00,000 | Credit Card Dues | 50,000 |

| Vehicles | 4,00,000 | — | — |

| Total Assets | 44,00,000 | Total Liabilities | 22,50,000 |

| Net Worth = 44,00,000 – 22,50,000 = ₹21,50,000 | |||

There is no single “right” number because it depends on lifestyle, income, and financial goals. But financial planners often use a simple benchmark:

By age 30: Aim for net worth equal to your annual salary. For example, if you earn ₹6 lakh per year, try to have at least ₹6 lakh in assets after deducting liabilities.

By age 40: Ideally, 2–3 times your annual salary. Example: earning ₹12 lakh per year → net worth should be ₹24–36 lakh.

By age 50: Around 5–6 times your annual salary. This is when your home loan may be close to repayment, and retirement savings should be growing.

By retirement (60+): At least 10 times your annual salary, preferably more, so that you can maintain the same lifestyle without active income.

Note: These benchmarks are general guidelines. If you live in a metro city with higher costs, your targets may need to be higher. On the other hand, in smaller towns, meeting these numbers may be easier. The key is to start investing early, avoid unnecessary debt, and steadily build assets over time.

Instead of calculating manually, a Net Worth Calculator online can:

Try our Free Net Worth Calculator to calculate your net worth instantly.

Q1. What is the formula for calculating net worth?

Net Worth = Assets – Liabilities. Assets include what you own (cash, investments, property), and liabilities include what you owe (loans, credit card dues). The difference shows your financial health – positive net worth means wealth creation, while negative means higher debt than assets.

Q2. What is considered an asset in net worth?

Assets are everything you own with value, such as bank savings, FDs, SIPs, stocks, retirement funds (EPF, PPF, NPS), property, gold, and vehicles. For businesses, it also includes equity or receivables. Always consider current market value, not original purchase price.

Q3. What is considered a liability?

Liabilities are obligations you must repay. These include home loans, car loans, personal or education loans, credit card dues, EMIs, overdrafts, and BNPL balances. In short, anything that reduces your wealth and creates repayment responsibility counts as a liability.

Q4. Can net worth be negative?

Yes, net worth can be negative if your debts are higher than your assets. For example, assets worth ₹7 lakh and liabilities worth ₹10 lakh result in –₹3 lakh net worth. This is common early in careers but can improve with savings and debt reduction.

Q5. How often should I calculate my net worth?

It’s best to calculate your net worth at least once a year, though every 6 months is ideal. Regular checks help track progress, show if your financial health is improving, and keep you focused on saving, investing, and repaying debt responsibly.

Q6. Is net worth only for the rich?

No, net worth is important for everyone. Even young professionals and middle-income earners benefit from knowing it. Tracking net worth helps you understand financial strengths and weaknesses, avoid unnecessary debt, and work toward long-term goals like buying a home or retirement.

Q7. Should I include depreciating assets like vehicles?

Yes, but only at their current resale value, not purchase price. For example, a car bought for ₹8 lakh may now be worth ₹4 lakh, which should be included. Items like gadgets or furniture lose value quickly and usually add little to net worth.

Q8. Does property always increase net worth?

Property usually adds to your net worth, but loans and market conditions matter. If you own it fully, the entire value is counted. If it’s on loan, only the portion you own adds. Property prices can rise, but they can also decline in weak markets.

Net Worth is a simple but powerful way to measure financial health. By learning how to calculate net worth, preparing a net worth statement, and tracking it regularly, you can make smarter decisions about saving, investing, and managing debt. For quick and accurate results, use an online Net Worth Calculator to see where you stand today.

Net Worth is the difference between what you own (assets) and what you owe (liabilities). It shows your real financial position. Whether you are an individual, a family, or a business, knowing how to calculate net worth helps you track progress, set financial goals, and plan for the future with clarity.

In this guide, we explain the net worth calculation formula, break down what counts as assets and liabilities, share practical examples, show a sample net worth statement, and also cover why using a Net Worth Calculator online is the fastest way to get accurate results.

| Factor | Details |

|---|---|

| Definition | Total Assets – Total Liabilities |

| Assets | Cash, investments, property, gold, vehicles, retirement funds |

| Liabilities | Loans, credit card dues, EMIs, mortgages |

| Formula | Net Worth = Assets – Liabilities |

| Type | Can be positive (healthy) or negative (more debt than assets) |

The formula is simple:

Net Worth = Total Assets – Total Liabilities

Assets:

Savings & Investments = ₹10,00,000

Property = ₹40,00,000

Vehicle = ₹5,00,000

Total Assets = ₹55,00,000

Liabilities:

Home Loan = ₹25,00,000

Car Loan = ₹3,00,000

Total Liabilities = ₹28,00,000

Net Worth = 55,00,000 – 28,00,000 = ₹27,00,000 (Positive)

Assets:

Savings & Investments = ₹2,00,000

Property = ₹5,00,000

Total Assets = ₹7,00,000

Liabilities:

Loans & Credit Card Debt = ₹10,00,000

Total Liabilities = ₹10,00,000

Net Worth = 7,00,000 – 10,00,000 = –₹3,00,000 (Negative)

A net worth statement shows assets and liabilities side by side for clarity. Here’s an example:

| Assets | Value (₹) | Liabilities | Value (₹) |

|---|---|---|---|

| Cash & Savings | 2,00,000 | Home Loan | 20,00,000 |

| Investments (SIP, FD, Stocks) | 8,00,000 | Car Loan | 2,00,000 |

| Property | 30,00,000 | Credit Card Dues | 50,000 |

| Vehicles | 4,00,000 | — | — |

| Total Assets | 44,00,000 | Total Liabilities | 22,50,000 |

| Net Worth = 44,00,000 – 22,50,000 = ₹21,50,000 | |||

There is no single “right” number because it depends on lifestyle, income, and financial goals. But financial planners often use a simple benchmark:

By age 30: Aim for net worth equal to your annual salary. For example, if you earn ₹6 lakh per year, try to have at least ₹6 lakh in assets after deducting liabilities.

By age 40: Ideally, 2–3 times your annual salary. Example: earning ₹12 lakh per year → net worth should be ₹24–36 lakh.

By age 50: Around 5–6 times your annual salary. This is when your home loan may be close to repayment, and retirement savings should be growing.

By retirement (60+): At least 10 times your annual salary, preferably more, so that you can maintain the same lifestyle without active income.

Note: These benchmarks are general guidelines. If you live in a metro city with higher costs, your targets may need to be higher. On the other hand, in smaller towns, meeting these numbers may be easier. The key is to start investing early, avoid unnecessary debt, and steadily build assets over time.

Instead of calculating manually, a Net Worth Calculator online can:

Try our Free Net Worth Calculator to calculate your net worth instantly.

Q1. What is the formula for calculating net worth?

Net Worth = Assets – Liabilities. Assets include what you own (cash, investments, property), and liabilities include what you owe (loans, credit card dues). The difference shows your financial health – positive net worth means wealth creation, while negative means higher debt than assets.

Q2. What is considered an asset in net worth?

Assets are everything you own with value, such as bank savings, FDs, SIPs, stocks, retirement funds (EPF, PPF, NPS), property, gold, and vehicles. For businesses, it also includes equity or receivables. Always consider current market value, not original purchase price.

Q3. What is considered a liability?

Liabilities are obligations you must repay. These include home loans, car loans, personal or education loans, credit card dues, EMIs, overdrafts, and BNPL balances. In short, anything that reduces your wealth and creates repayment responsibility counts as a liability.

Q4. Can net worth be negative?

Yes, net worth can be negative if your debts are higher than your assets. For example, assets worth ₹7 lakh and liabilities worth ₹10 lakh result in –₹3 lakh net worth. This is common early in careers but can improve with savings and debt reduction.

Q5. How often should I calculate my net worth?

It’s best to calculate your net worth at least once a year, though every 6 months is ideal. Regular checks help track progress, show if your financial health is improving, and keep you focused on saving, investing, and repaying debt responsibly.

Q6. Is net worth only for the rich?

No, net worth is important for everyone. Even young professionals and middle-income earners benefit from knowing it. Tracking net worth helps you understand financial strengths and weaknesses, avoid unnecessary debt, and work toward long-term goals like buying a home or retirement.

Q7. Should I include depreciating assets like vehicles?

Yes, but only at their current resale value, not purchase price. For example, a car bought for ₹8 lakh may now be worth ₹4 lakh, which should be included. Items like gadgets or furniture lose value quickly and usually add little to net worth.

Q8. Does property always increase net worth?

Property usually adds to your net worth, but loans and market conditions matter. If you own it fully, the entire value is counted. If it’s on loan, only the portion you own adds. Property prices can rise, but they can also decline in weak markets.

Net Worth is a simple but powerful way to measure financial health. By learning how to calculate net worth, preparing a net worth statement, and tracking it regularly, you can make smarter decisions about saving, investing, and managing debt. For quick and accurate results, use an online Net Worth Calculator to see where you stand today.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.