The Public Provident Fund (PPF) is a popular long-term savings scheme with a 15-year lock-in. But what if you need to withdraw your entire balance before maturity? This is possible through premature closure of PPF account, but only under strict rules and conditions. In this article, we’ll explain the PPF premature closure rules, the process to close your account, the conditions under which it is allowed, and real-life examples to make it simple.

| Aspect | Details |

|---|---|

| Eligibility | After completing 5 financial years from account opening |

| Allowed Reasons | Higher education, serious medical treatment, or change of residency (NRI) |

| Penalty | Interest rate reduced by 1% from the actual rate earned |

| Tax Treatment | Maturity proceeds remain tax-free (EEE status continues) |

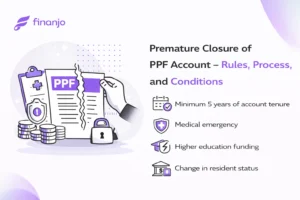

The government allows premature closure of PPF account only after the completion of 5 financial years. Even then, closure is allowed only for specific reasons mentioned below:

Here are the steps to close your PPF account before maturity:

Suppose you opened a PPF account in FY 2018–19 and want to close it in FY 2024–25 (after 6 years) for higher education expenses.

So, you still receive your savings, but the interest loss reduces your final corpus.

It simply means closing your PPF account before the full 15 years are over and taking out the money earlier than planned.

Not really. PPF is meant for long-term savings, so early closure is allowed only in certain genuine situations.

You can apply for premature closure only after 5 years have passed since you opened the account.

Early closure is allowed if there’s a real need, like:

Yes. You’ll need to submit documents like medical reports, hospital bills, college admission letters, or proof of NRI status.

You won’t lose your principal, but the interest will be slightly reduced as a penalty for early closure.

The interest for all completed years is recalculated at 1% lower than the regular PPF rate.

You’ll have to visit the bank or post office where your PPF account is held, fill out a form, and submit your documents.

In most cases, no. Since documents need to be checked, banks usually ask you to come in person.

Once everything is verified and approved, the amount is generally credited within a few working days.

Yes. Partial withdrawals are allowed after a certain time and are often a better option if you need only part of the money.

No. PPF remains completely tax-free, even if you close it before maturity.

Yes, but only for valid reasons like medical or education needs, and the guardian has to apply.

Yes. If your reason doesn’t match the rules or documents are missing, the bank can reject the request.

Only if you really have to. PPF is one of the safest and most stable savings options, so early closure should be the last choice.

The Public Provident Fund (PPF) is a popular long-term savings scheme with a 15-year lock-in. But what if you need to withdraw your entire balance before maturity? This is possible through premature closure of PPF account, but only under strict rules and conditions. In this article, we’ll explain the PPF premature closure rules, the process to close your account, the conditions under which it is allowed, and real-life examples to make it simple.

| Aspect | Details |

|---|---|

| Eligibility | After completing 5 financial years from account opening |

| Allowed Reasons | Higher education, serious medical treatment, or change of residency (NRI) |

| Penalty | Interest rate reduced by 1% from the actual rate earned |

| Tax Treatment | Maturity proceeds remain tax-free (EEE status continues) |

The government allows premature closure of PPF account only after the completion of 5 financial years. Even then, closure is allowed only for specific reasons mentioned below:

Here are the steps to close your PPF account before maturity:

Suppose you opened a PPF account in FY 2018–19 and want to close it in FY 2024–25 (after 6 years) for higher education expenses.

So, you still receive your savings, but the interest loss reduces your final corpus.

It simply means closing your PPF account before the full 15 years are over and taking out the money earlier than planned.

Not really. PPF is meant for long-term savings, so early closure is allowed only in certain genuine situations.

You can apply for premature closure only after 5 years have passed since you opened the account.

Early closure is allowed if there’s a real need, like:

Yes. You’ll need to submit documents like medical reports, hospital bills, college admission letters, or proof of NRI status.

You won’t lose your principal, but the interest will be slightly reduced as a penalty for early closure.

The interest for all completed years is recalculated at 1% lower than the regular PPF rate.

You’ll have to visit the bank or post office where your PPF account is held, fill out a form, and submit your documents.

In most cases, no. Since documents need to be checked, banks usually ask you to come in person.

Once everything is verified and approved, the amount is generally credited within a few working days.

Yes. Partial withdrawals are allowed after a certain time and are often a better option if you need only part of the money.

No. PPF remains completely tax-free, even if you close it before maturity.

Yes, but only for valid reasons like medical or education needs, and the guardian has to apply.

Yes. If your reason doesn’t match the rules or documents are missing, the bank can reject the request.

Only if you really have to. PPF is one of the safest and most stable savings options, so early closure should be the last choice.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.