The Public Provident Fund (PPF) requires you to deposit at least ₹500 every financial year to keep the account active. If you fail to deposit the minimum amount in any year, your account becomes inactive (discontinued). An inactive account does not allow fresh deposits until revived. However, the good news is that you can reactivate your PPF account by following certain rules.

Note: Even if inactive, the money already in the account continues to earn interest until maturity.

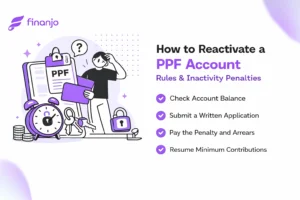

To reactivate your account, you must:

Once done, your account will be restored, and you can start making fresh deposits again.

Suppose you opened a PPF account in April 2018 but did not deposit anything in FY 2020-21 and FY 2021-22.

Once you pay this amount, your account will be reactivated.

If your PPF account has gone inactive, don’t stress. Getting it back on track is actually quite easy.

First, visit the bank branch or post office where your PPF account is held. PPF reactivation usually can’t be done online, so you’ll need to go in person.

Tell the staff that your PPF account has become inactive and you want to revive it. They’ll either give you a revival form or ask you to submit a simple written request with your account details.

To reactivate the account, you’ll need to pay:

You can pay both amounts together during the revival process.

Once everything is submitted and paid, the bank or post office will process your request. After confirmation, your PPF account becomes active again, and you can continue investing like before.

An inactive (or discontinued) PPF account is one where you did not deposit the minimum ₹500 in a financial year. Once this happens, the account stops accepting fresh deposits until it is revived.

Your PPF account becomes inactive if no contribution is made in a financial year. Even missing the minimum deposit for just one year can make the account inactive.

No. Fresh deposits are not allowed in an inactive PPF account. You must first reactivate the account by paying the required penalty and minimum deposit.

Yes. The existing balance continues to earn interest even if the account is inactive. However, you won’t be able to enjoy full PPF benefits until it is revived.

You can reactivate your account by:

No, there is no strict deadline. You can revive your inactive PPF account any time before maturity by following the revival process.

If you don’t revive it:

Withdrawals are usually restricted in an inactive account. Full withdrawal and loan benefits are available only after the account is reactivated.

No. You can revive the account in one go by paying the total penalty and minimum deposit for all the missed years together.

No, an inactive PPF account does not get automatically closed. It continues till maturity, but with limited flexibility unless revived.

The Public Provident Fund (PPF) requires you to deposit at least ₹500 every financial year to keep the account active. If you fail to deposit the minimum amount in any year, your account becomes inactive (discontinued). An inactive account does not allow fresh deposits until revived. However, the good news is that you can reactivate your PPF account by following certain rules.

Note: Even if inactive, the money already in the account continues to earn interest until maturity.

To reactivate your account, you must:

Once done, your account will be restored, and you can start making fresh deposits again.

Suppose you opened a PPF account in April 2018 but did not deposit anything in FY 2020-21 and FY 2021-22.

Once you pay this amount, your account will be reactivated.

If your PPF account has gone inactive, don’t stress. Getting it back on track is actually quite easy.

First, visit the bank branch or post office where your PPF account is held. PPF reactivation usually can’t be done online, so you’ll need to go in person.

Tell the staff that your PPF account has become inactive and you want to revive it. They’ll either give you a revival form or ask you to submit a simple written request with your account details.

To reactivate the account, you’ll need to pay:

You can pay both amounts together during the revival process.

Once everything is submitted and paid, the bank or post office will process your request. After confirmation, your PPF account becomes active again, and you can continue investing like before.

An inactive (or discontinued) PPF account is one where you did not deposit the minimum ₹500 in a financial year. Once this happens, the account stops accepting fresh deposits until it is revived.

Your PPF account becomes inactive if no contribution is made in a financial year. Even missing the minimum deposit for just one year can make the account inactive.

No. Fresh deposits are not allowed in an inactive PPF account. You must first reactivate the account by paying the required penalty and minimum deposit.

Yes. The existing balance continues to earn interest even if the account is inactive. However, you won’t be able to enjoy full PPF benefits until it is revived.

You can reactivate your account by:

No, there is no strict deadline. You can revive your inactive PPF account any time before maturity by following the revival process.

If you don’t revive it:

Withdrawals are usually restricted in an inactive account. Full withdrawal and loan benefits are available only after the account is reactivated.

No. You can revive the account in one go by paying the total penalty and minimum deposit for all the missed years together.

No, an inactive PPF account does not get automatically closed. It continues till maturity, but with limited flexibility unless revived.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.